ACM Update 30-01-23

Rishi Sunak joins the 100 club this week, already achieving more than double the days in power his infamous predecessor Liz Truss managed. But UK news hasn’t been pretty, with widespread industrial action and the saga surrounding Nadhim Zahawi in recent weeks.

In the markets, GBP has largely been trading sideways, without any major direction. This week sees interest rate announcements from the “big three”, the Federal Reserve, Bank of England and European Central Bank. With US Non-Farm Payrolls to close out the week, we could well see a bumpy start to February.

A busy week for UK data and unwanted political headlines last week for Nadhim Zahawi. The very short-lived Chancellor was removed from his post after “serious tax breaches”, further denting the Conservative party image. The current Chancellor, Jeremy Hunt, ironically confirmed last week that significant tax cuts in the upcoming budget were “unlikely”. News also broke that December’s UK government borrowing rose to its highest since records began in 1993. Energy bill support and higher interest repayments on debt were major factors.

UK car production has also fallen to its lowest since 1956, according to annual figures. Car firms are warning that the country is not doing enough to attract manufacturing firms. The number of vehicles produced has fallen every year since 2016, a drop of 50%. Indeed, manufacturing PMI data released last week came in at 46.7 for January, demonstrating contraction, albeit not as bad as forecast. The services sector fared slightly better at 48.0, still in contraction and under expectation.

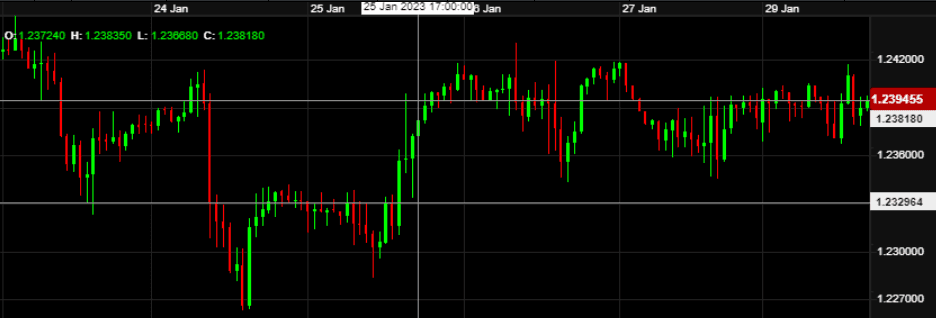

A gloomy UK picture overall, but very little by the way of movement for GBP-EUR last week, as shown in the chart below:

Over in the US we also had Services and Manufacturing data to digest. These came in at 46.6 & 46.8 respectively, still demonstrating contraction. The main release was advance GDP (quarter on quarter) for Q4, which came in at 2.9% and the previous period also revised up to 3.2%. A reasonably stable week for the Dollar against its peers.

This week though sees the two biggest pieces of US data, with an interest rate announcement from the Federal Reserve and Non-Farm Payrolls. For last week, relatively quiet as illustrated in the chart below:

Equally, a pretty quiet week for the Eurozone, resulting in a narrow trading band for EUR-USD. A mixed bag of PMI data as well as a speech from Christine Lagarde were the main events. Once again the ECB chief maintained the narrative of the bank doing whatever necessary to get inflation back to 2%. She reaffirmed that rates will continue to “rise significantly and at a steady pace”.

Elsewhere, the Bank of Canada hiked interest rates to 4.5%. This was only a 25 basis point hike and demonstrates a considerable slowdown in rate rises, having now gone 100-75-50 and now 25 over their last four meetings.

Australian inflation hit its highest level since 1990 in the quarter to December. The figure came in at 7.8% on Wednesday (expected 7.6%), driving GBP-AUD to its lowest since mid-October. As is the norm currently, this was driven by higher electricity, food and fuel prices.

The week ahead:

Tuesday – UK Mortgage Approvals (09:30 UK time), Canadian GDP m/m (13:30)

Wednesday – Nationwide UK House Prices (07:00), EU/UK/US/CAN Manufacturing Data (08:15-15:00), ADP Jobs Data (13:15), Federal Reserve Rate Announcement (19:00) & Press Conference (19:30).

Thursday – Bank of England Rate Announcement (12:00), ECB Rate Announcement (13:15) & Press Conference (13:45)

Friday – Bank of England Chief Economist, Huw Pill’s speech 12:15, US Non-Farm Employment (13:30)

So a very action-packed week to come with the Federal Reserve the first of the major events on Wednesday evening. A 50 basis point hike should be a foregone conclusion based on recent Fed narrative. Anything outside of this, or comments in the subsequent press conference suggesting a change of tact, will cause volatility.

The Bank of England are still essentially playing “chase the Fed” with their own rate announcements. Expect a further 50 basis points here too and likely the same from the European Central Bank also. The week closes out with Non-Farm Payrolls (employment) data on Friday afternoon.

After a calm week last week of circa 1% movement on most majors, we could well see considerably more than that in the week ahead. Any clients with upcoming requirements that percentage points worth of movement would make a major impact to, should look to reach out to the team this week to discuss relevant solutions.

Have a great week.