ACM Update 28-03-22

A far quieter week than those of late in terms of major data releases last week, with UK inflation being the main headline-grabber. Inflation is now running at its highest level in 30 years at 6.2%. Again, it is worth stressing that these figures are for February, at which point the recent incline in fuel prices had only just started. A further sobering thought is that the energy price cap is being raised by a spectacular 54% as of this Friday 1st April. If only it was an April Fools’ prank…

We also had UK retail sales for February released last week, which showed an unexpected drop month on month of -0.3%. The January number was 1.9% and expectations were for 0.6% growth in February, but it seems the recent cost of living increases are causing caution in spending habits. Stagnant growth, stalling retail sales and soaring inflation…. Its beginning to look a lot like stagflation.

In his Spring statement, Chancellor Rishi Sunak pledged action to target the soaring cost of living in Britain. A rise in the National Insurance threshold, basic rate tax cuts (20 to 19%) to be brought in by the end of 2024 and an immediate 5p per litre reduction in fuel duty were some of the main takeaways. The Office for Budget Responsibility (OBR) have realigned their expectations for economic growth from 6% for 2022, down to 3.8%. They also see inflation averaging 7.4% this year, having suggested a mere 4% six months ago.

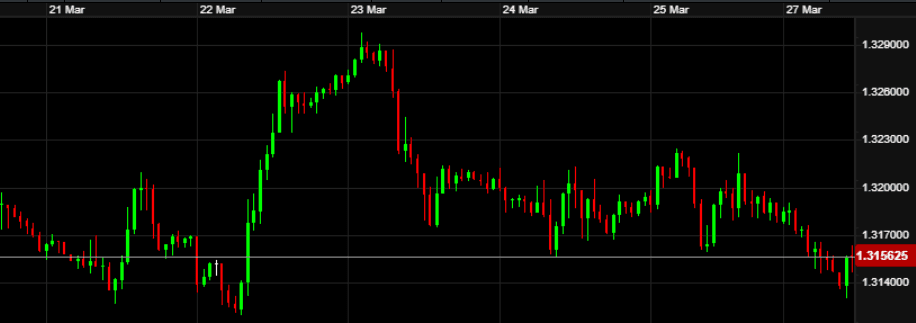

The impact these events had on GBP versus the Euro last week were varied, causing the pair to bounce along either side of 1.20 throughout the week. The total range of movement was circa 1.5% and can be seen in the chart below:

In the EU, most of the focus is still rightly on the Russian invasion of Ukraine, very much on their doorstep. Christine Lagarde currently doesn’t see a risk of stagflation for the bloc, but said in an interview last week that the ECB have calculated various different scenarios depending on events in Ukraine. They forecast growth of 3.7% for 2022, but agree this could be as low as 2.3%. Perhaps a slightly confusing statement being that the ECB “remain very attentive to prevailing uncertainties”.

Aside from US unemployment figures continuing to drop, the main talking points stateside last week came from Jerome Powell. The Fed are forecast for a further seven interest rate hikes this year, with the Fed Governor stating they may need to get more “aggressive” with rate hikes, as inflation is “much too high”. With only six Fed meetings remaining this year, the May meeting is currently 50:50 for a 50-basis point hike.

The Dollar is still benefitting from its “safe haven” status as the situation in Ukraine continues. The near-certainty of further interest rate rises on both sides of the Atlantic soon are keeping the pair finely poised between 1.30 and 1.33 in recent weeks. Dollar strength is likely to remain for some time to come, so those needing to buy USD over the coming weeks should reach out to the team to protect your exposure. Recent moves on the pair can be seen below:

Elsewhere, commodity-backed currencies remain very strong as oil prices jump again. In Australia, concerns are also rising around a spike in inflation which has compounded the strength of the AUD. These have led to the potential of an interest rate rise come sooner than had previous been expected, boosting the investment attractiveness of the AUD. A speech mid-week from RBA Governor Philip Lowe added further fuel to the fire on that front.

This week:

Monday – Bank of England Governor Andrew Bailey speech (12pm UK time)

Tuesday – UK Mortgage Approvals (9:30am)

Wednesday – US final GDP QoQ (1:30pm)

Thursday – UK final GDP QoQ (7am) – Month & Quarter End

Friday – UK/EU/CAN/US Manufacturing data (all day) & US Non-Farm Payrolls (1:30pm)

Most of the events this coming week are going to revolve around Thursday and Friday. That is not to say that the rest of the week will be quiet though. If you have visibility of your upcoming currency exposures for Q2, now is a vital time to look at hedging to protect yourself.

Speaking of which, with month end and quarter end on Thursday, there is certainly potential for sizeable movements in the afternoon as traders close out positions and take profits. Sterling-Dollar could well see some substantial movements after those we have seen thus far for various reasons in the first quarter.

Friday brings the biggest data release of the month in the US, in the shape of Non-Farm Payrolls. Can the US add close to a further half a million jobs again this month? Potentially so if other recent releases are correct. A busy end to the week is in store, so get in touch with me or anyone in the Aston team if you don’t want to be taken for an April Fool by the FX markets!

Have a great week.